Moving Averages (MAs) are the bread and butter of technical analysis. Whether you are building a simple trend-following bot in Python or a complex Pine Script strategy, the way you implement these indicators determines the difference between a profitable system and a “repainting” disaster.

To move beyond basic tutorials, developers must understand the nuances of calculation, data handling, and signal confirmation. Here is how to use moving averages correctly in your strategy code.

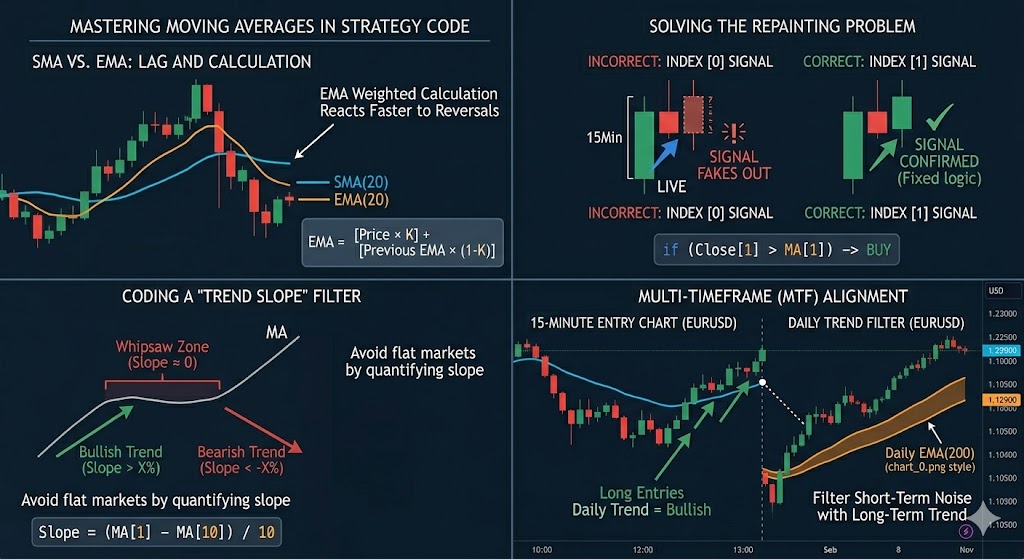

1. SMA vs. EMA: Choosing the Right Foundation

The first step is selecting the mathematical model that fits your strategy’s objective.

- Simple Moving Average (SMA): Calculates the arithmetic mean of a given set of prices. It is best for identifying long-term institutional support and resistance levels.

- Exponential Moving Average (EMA): Places more weight on recent price data. Because it reduces lag, it is the preferred choice for traders looking to capture short-term momentum shifts.

Coding Tip: When coding an EMA, ensure your script has enough “warm-up” data. Since EMAs use previous values in their calculation, an EMA calculated with 50 bars of history will look different than one calculated with 500 bars.

2. Solving the “Repainting” Problem

The most common mistake in strategy coding is calculating signals based on the current, open candle (Index 0). In live markets, the “Close” price of a live candle fluctuates until the timer hits zero. If your code triggers a buy because the price crossed the MA mid-candle, that signal might disappear by the time the candle actually closes.

The Professional Standard: Always reference the completed candle (Index 1). In your code, your logic should look like this: If Close[1] > MovingAverage[1] then Signal = Buy

This ensures that your backtest results match your live trading reality.

3. Implementing a “Look-Back” for Trend Slope

Simply checking if the price is above or below a Moving Average isn’t enough to confirm a trend. A “flat” moving average indicates a ranging market where crossovers are likely to be false signals.

To code a “Trend Filter,” calculate the slope of the MA. You can do this by comparing the current MA value to its value five or ten bars ago.

- Bullish:

MA[1] > MA[10] - Neutral:

MA[1] == MA[10](within a small buffer) - Bearish:

MA[1] < MA[10]

4. Handling the Data Warm-up Period

If your strategy uses a 200-period Moving Average, your code cannot generate a valid trade on the first 199 bars of data. If you don’t account for this, your code may throw errors or return “Null” values.

Always include a safety check at the beginning of your execution loop: if (bar_index < 200) return;

5. Multi-Timeframe (MTF) Integration

Professional strategy code often uses a “Higher Timeframe” filter. For example, a 15-minute mean-reversion strategy is much more effective if it only takes “Long” trades when the price is above the 200-period EMA on the Daily chart.

By coding your script to request data from a higher timeframe, you align your algorithm with the “Big Picture” trend, significantly increasing your win rate.

Conclusion

Using moving averages in code is about more than just calling a library function. It requires a disciplined approach to data indexing, slope analysis, and timeframe alignment. By implementing these professional standards, you can transform a lagging indicator into a leading edge.

Click here If you are looking for Professional Custom Trading Software Development Services