VWAP, or Volume Weighted Average Price, is one of the most widely used intraday indicators for measuring the average traded price of an instrument based on both price and volume. Many traders use VWAP as a dynamic reference level for trend direction, mean reversion, institutional activity, and intraday support or resistance.

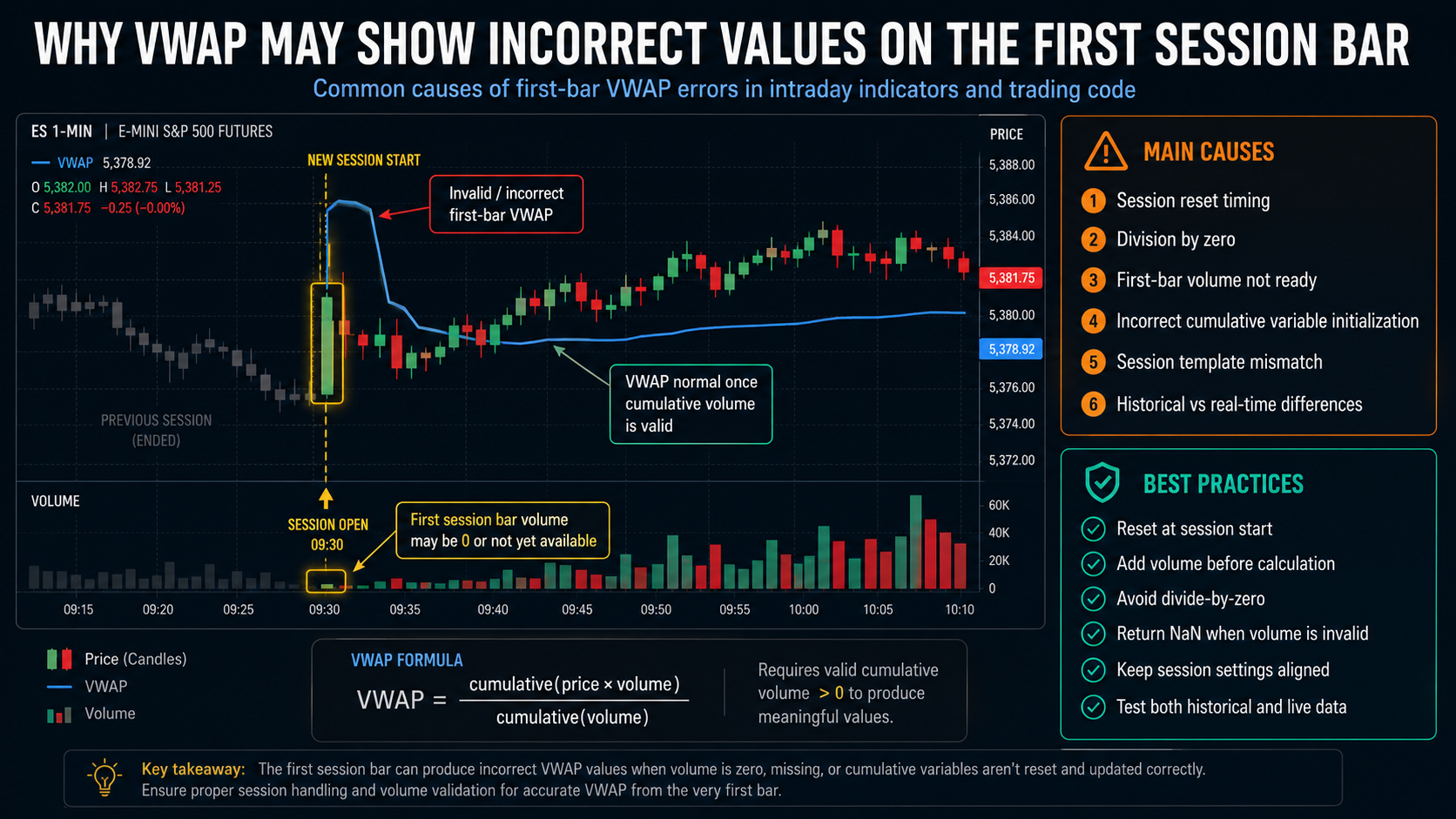

However, one common issue traders and developers may notice is that VWAP can sometimes display an incorrect value on the first bar of a new trading session. In some cases, the first session bar may show an extremely large value, zero, NaN, infinity, or a value that does not match the expected chart behavior.

This issue is usually not caused by VWAP itself. It is most often related to how the indicator initializes, resets, and calculates session-based values.

What VWAP Measures

VWAP is calculated by dividing cumulative price-volume value by cumulative volume:

VWAP = Cumulative Price × Volume / Cumulative Volume

Because VWAP depends on cumulative session data, it must restart at the beginning of each new session. This reset process is where many first-bar calculation problems occur.

Why the First Session Bar Can Be Incorrect

1. Session Reset Timing

VWAP usually resets when a new trading session begins. If the indicator resets cumulative price-volume and cumulative volume too early or too late, the first bar may calculate using incomplete or incorrect values.

For example, if the session reset happens before the first bar has valid volume, VWAP may temporarily calculate with zero cumulative volume.

2. Division by Zero

A common programming issue occurs when cumulative volume is zero on the first session bar. Since VWAP divides by cumulative volume, this can create an invalid result.

This may cause the indicator to display:

- NaN

- Infinity

- Zero

- An unusually large or incorrect value

A properly coded VWAP should check whether cumulative volume is greater than zero before performing the calculation.

3. First Bar Volume Is Not Fully Available Yet

On real-time charts, the first bar of a session may still be forming. Depending on the platform and calculation mode, the volume value may not be fully updated when the indicator first calculates.

This is especially common when the script runs on each tick instead of only after the bar closes.

4. Incorrect Initialization of Cumulative Variables

VWAP requires cumulative variables such as:

- Cumulative volume

- Cumulative price-volume

- Session start flag

- Previous session state

If these variables are not initialized correctly, the first session bar may inherit values from the previous session or start with invalid data.

5. Session Template or Trading Hours Mismatch

Different chart platforms use different session templates, trading hours, and data settings. If the VWAP indicator uses one session definition while the chart uses another, the first bar may not align correctly.

This can happen with futures, stocks, forex, and extended-hours data.

For example, VWAP may reset at the regular session open, while the chart includes pre-market or overnight data.

6. Multi-Timeframe Data Issues

If VWAP is calculated using a secondary data series or higher timeframe, the first session bar may not have synchronized data yet. This can cause the VWAP value to appear delayed, incorrect, or missing.

Multi-timeframe VWAP calculations require careful handling of bar updates and session boundaries.

7. Historical vs Real-Time Calculation Differences

Some platforms process historical bars differently from real-time bars. A VWAP value may look correct after reloading the chart but appear incorrect during live market updates.

This usually means the indicator logic behaves differently during real-time initialization than it does during historical calculation.

How to Prevent Incorrect VWAP Values on the First Bar

To avoid first-bar VWAP errors, developers should use protective logic in the calculation.

Important safeguards include:

- Reset cumulative values exactly at the session start

- Add volume before calculating VWAP

- Avoid dividing by zero

- Return NaN when volume is not available

- Confirm that the chart and indicator use the same session template

- Handle real-time and historical bars consistently

- Check whether the bar is the first bar of the session before applying logic

A safer VWAP calculation should only produce a value when cumulative volume is valid. If cumulative volume is zero, the indicator should not plot a misleading value.

Why This Matters for Trading Strategies

An incorrect VWAP value on the first session bar can affect more than just the visual chart. It can also impact automated trading strategies, alerts, scanners, and signal filters.

For example, if a strategy checks whether price is above or below VWAP, an invalid first-bar VWAP value may cause:

- False trade signals

- Missed entries

- Incorrect trend filters

- Unreliable backtesting results

- Differences between historical and live performance

This is why VWAP initialization should be handled carefully, especially in automated trading systems.

Best Practice for VWAP Indicator Development

When coding a VWAP indicator, the first session bar should be treated as a special case. The indicator should reset the session values, confirm valid volume, and only then calculate VWAP.

If valid cumulative volume is not available, it is better to return NaN instead of displaying an incorrect value. This prevents misleading chart output and helps strategies avoid false signals.

Conclusion

VWAP may show incorrect values on the first session bar because of session reset timing, zero volume, incomplete real-time data, incorrect variable initialization, or trading-hour mismatches. Since VWAP is a cumulative session-based indicator, the first bar requires careful handling.

For accurate VWAP calculations, the indicator should reset properly at the session start, validate cumulative volume, avoid division by zero, and ensure that chart session settings match the indicator logic.

Correctly handling the first session bar improves chart accuracy, reduces false signals, and makes VWAP more reliable for both discretionary trading and automated strategies.